Too Big to Fail 2.0

How Your Retirement Money Is Tied to the Riskiest Corner of Finance

What would you buy with two trillion dollars?

You could buy

Apple

Coca-Cola

Nike

McDonalds

and still have money left over.

It’s an amount of money so huge it’s hard to even imagine.

Yet, a financial market of this very size has quietly grown up in the shadows of our economy and it origins begin before the last financial crisis.

In the years before 2008, a dangerous idea took hold in the financial world.

The experts believed they had tamed risk by chopping it up, repackaging it, and selling it in the shadows of the traditional banking system. They created trillions of dollars in complex products based on risky mortgages, all while assuring the world they were safe.

We all know how that story ended.

Today, a new shadow system, eerily similar in its secrecy and explosive growth, has taken its place.

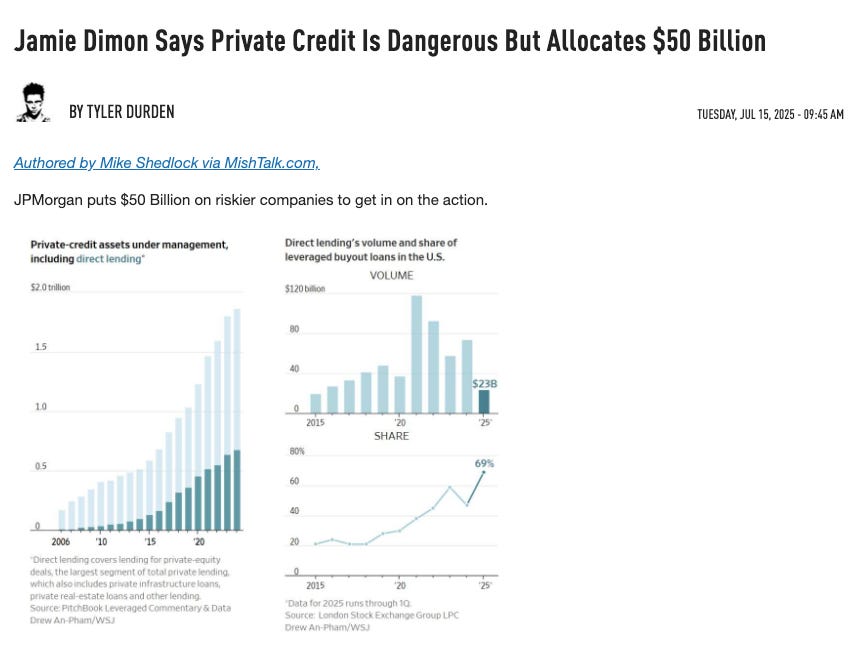

It’s called private credit, and at over $2 trillion in size, it is now so large that regulators are beginning to ask the one question that should make us all uneasy: have we already created financial crisis in plain sight?

Private credit is, at its core, lending that happens outside the publicly regulated banking system. To understand its explosive rise, we have to go back to the ashes of the 2008 meltdown.

In response to the crisis, the U.S. government passed the Dodd-Frank Act, a sweeping set of regulations designed to prevent another catastrophe. A key part of these new rules forced big banks to hold much more capital in reserve designed to keep a bigger cash cushion on hand in case their loans went bad.

This made making riskier loans to medium-sized or highly indebted companies far less profitable for them. Faced with a choice between a low-profit loan and a safer investment, banks predictably chose safety.

This created a massive credit vacuum.

Thousands of perfectly viable companies, the backbone of the economy, suddenly found it much harder to get a loan to expand a factory, hire more workers, or develop a new product.

Into this void stepped a new class of lender: non-bank financial institutions, or what we now call the private credit market.

These entities run by giant asset managers like Apollo, Blackstone, and KKR were not banks, so they weren’t subject to the same strict capital rules.

They could raise money from large investors like pension funds and insurance companies and lend it out on their own terms, charging higher interest rates to compensate for the higher risk.

The model was a hit, and money poured in.

A market that was a few hundred billion dollars a decade ago has now swelled to over $2 trillion, a five-fold increase that has made it a central pillar of corporate finance.

The Perfect Partnership That Fuels the Market

The secret market of private credit grew so big, so fast, because of its powerful partnership with another area of finance: private equity.

Think of private equity firms as professional home flippers, but instead of houses, they flip entire companies.

Their goal is to buy a company, make it more valuable, and then sell it a few years later for a big profit. To do this, they need to borrow a lot of money.

The main tool they use is called a “leveraged buyout.”

The word leverage here just means using borrowed money.

It works a bit like buying a rental property. Let’s say you want to buy a $200,000 rental house. You might only use $40,000 of your own money and get a $160,000 mortgage from the bank. That mortgage is the leverage.

If the house’s value goes up to $250,000, your small $40,000 investment has made you a $50,000 profit.

You used the bank’s money to make your own return much bigger.

Private equity firms do the same thing with companies.

If they want to buy a business for $100 million, they might only use $30 million of their own and borrow the other $70 million.

Where do they borrow it from?

Increasingly, their favorite place is the private credit market. Private credit lenders can move fast and are willing to lend huge sums of money for these deals. This partnership has become a giant engine for the economy.

Private equity firms have trillions of dollars of their own cash, called “dry powder,” that they need to invest. To invest it, they will need to borrow even more money from private credit funds. This ensures the secret market will keep growing. But it also means that the companies they buy are loaded up with huge amounts of debt, which makes them very fragile.

Problem #1: Flying Blind in a Dark Room

One of the biggest worries that keeps financial experts up at night is how secretive the private credit market is. Because the loans are private deals between a fund and a company, almost none of the details are made public. This creates a huge blind spot in our economy.

When a company is public, meaning its stock is traded on an exchange like the New York Stock Exchange, it has to share its financial information every three months. Everyone can see if the company is making money or losing money.

This transparency is important.

It allows us to see if a company is healthy.

But the companies funded by private credit are private.

They don’t have to share this information.

This makes it almost impossible for anyone on the outside, including the people who regulate our economy, to know how much risk is building up. Trying to understand the health of the private credit market is like a doctor trying to figure out if a patient is sick without being able to run any tests or ask any questions.

You might only find out there is a problem when the patient collapses.

This secrecy also affects how loans are valued.

When you own a stock, like a share of Apple, you know exactly what it’s worth every second of the day because its price is public.

This is called “marking to market.”

But a private credit loan has no public price.

The person who decides what the loan is worth is the manager of the fund that made the loan.

This is called “marking to model.”

This creates a serious conflict.

The fund manager gets paid a fee based on the total value of the loans they manage. If they admit that a loan has gone down in value because the borrowing company is struggling, their own pay gets cut.

This gives them a big reason to pretend everything is fine and keep the loan valued at its original price, even when trouble is brewing. This hides the problems until it’s too late.

Problem #2: Taking Away the Safety Rules

Another huge risk comes from a change in the loan agreements themselves. For hundreds of years, loans came with safety rules for the borrower, called covenants. These rules are like the ones parents set for a teenager who wants to borrow the family car.

Lets say a parent says, “You can use the car as long as you keep your grades above a B and you’re home by your 11 PM curfew.”

These rules are the covenants.

If the teen’s grades slip to a C, the parent can step in and take away the car keys.

The parent doesn’t have to wait for the teen to get into a serious accident to act. The broken rule is an early warning sign that lets the parent prevent a bigger disaster.

Traditional loan covenants work the same way.

A covenant might say a company’s debt cannot be more than five times what it earns in a year. If the company has a bad year and its debt level gets too high, the lender can step in right away and demand changes.

But in the private credit market, the competition to make loans is so intense that most of these safety rules have been thrown out.

Lenders now offer “covenant-lite” loans to win business.

These are loans with no early warning systems.

It’s like a parent giving their teen the car keys with no rules about grades or curfew. The parent might not find out there’s a problem until they get a call from the police saying their child has crashed the car.

With a covenant-lite loan, the lender often has very little power to do anything until the company actually stops paying its bills. By that point, the company is already in a full-blown crisis, and the chances of the lender getting its money back are much, much lower.

Problem #3: The First Signs of Trouble Are Here

For a long time, the private credit market seemed perfect. It offered high returns for investors, and very few companies were failing to pay back their loans. But now, with higher interest rates making debt more expensive, we are starting to see the first cracks appear.

One major warning sign is something called Payment-in-Kind, or PIK interest. A healthy company pays the interest on its debt with the cash it makes from selling its products or services.

But what if a company doesn’t have enough cash?

A PIK loan lets them “pay” their interest by just adding it to their total debt.

It’s like having a $1,000 credit card bill with a $20 interest charge.

Instead of paying the $20 in cash, the bank says you can just add it to your balance.

Now you owe $1,020, and next month, you’ll be paying interest on that higher amount. Your debt grows on its own, even if you don’t spend another dollar.

More and more companies in the private credit world are using PIK interest. It’s a clear sign they are struggling to generate enough cash.

Another warning light is the interest coverage ratio.

This simply measures if a company is earning enough money to pay the interest on its debt. If a company earns $3 million and its interest bill is $1 million, its coverage ratio is 3.

This is healthy.

But if its earnings drop to $900,000, its coverage ratio is now less than 1. This means the company isn’t even making enough money to cover its interest payments.

We are now seeing increasing number of companies funded by private credit having a coverage ratio of less than 1.

These are often called “zombie companies” because they are not really alive.

They are just stumbling along, kept from collapse only by borrowing more money to pay the interest on their old money.

We are also starting to see more companies begin to enter this zombie stage as consumers cut back on spending.

Problem #4: A Ship That Has Never Sailed in a Hurricane

The scariest part of this whole story might be this: the giant, two-trillion-dollar private credit market has never been through a real, painful recession. It grew up in a time of mostly good economic weather. The only storm it faced was the short one caused by the COVID-19 pandemic in 2020.

But the government quickly stepped in with so much financial aid that it was like sending a rescue fleet to save every ship, big or small.

As a result, we have a huge, important part of our financial system that has never been truly stress-tested.

We have no idea how it will behave in a real economic hurricane, a time when people lose their jobs, stop spending money, and company profits disappear for a year or more.

How will all these debt-filled “zombie companies” survive?

What will happen when thousands of covenant-lite loans all start to go bad at the same time?

No one knows the answer, because it has never happened before.

This huge unknown is a risk all by itself.

How a Secret Problem Could Become Everyone’s Problem

You might think that a problem in a secret market would stay secret. But the private credit world is deeply connected to the regular financial system we all rely on. A fire that starts there could easily spread and burn down the whole neighborhood.

The first connection is to the big banks.

Even though banks don’t make these risky loans anymore, they do lend huge amounts of money to the private credit funds themselves.

The funds use these bank loans like a giant credit card. If a lot of companies start failing to pay back their private credit loans, the funds will get desperate for cash. They will all rush to their banks at the same time to use their credit lines. This could put a sudden, massive strain on the banking system, the very system the new rules were supposed to protect.

The second connection is even more personal.

Who are the big investors that give private credit funds their money?

Two of the biggest groups are pension funds and insurance companies.

Pension funds manage the retirement savings for millions of people like teachers, police officers, and government workers.

Insurance companies use their money to pay for everything from car crashes to house fires. These groups invested in private credit because it promised safe, steady returns to help them pay for our retirements and our insurance claims.

If the private credit market collapses and loses hundreds of billions of dollars, the losses will be passed on to them. This could put the retirement security of millions of people at risk.

This all feels very familiar.

The story of 2008 was about how risks hidden in one corner of the financial world could suddenly explode and hurt everyone.

We were promised that this would not happen again.

Yet, in solving the problems of the old system, we have potentially created a new, two-trillion-dollar problem.

Private credit has become an essential engine for business, but it is an engine running without a modern safety inspection.

The warning lights are starting to flash, and the world’s regulators are only now scrambling to figure out how to avoid another crisis.

The real test is coming, and our collective financial future may depend on whether we have truly learned the lessons of our past, or if we are doomed to repeat them.

This is the third piece in a four-part series on the ‘Four Economic Horsemen of the Apocalypse’ focused on the systemic risks facing the US and Global Economy in 2025.