The Quiet Collapse of the American Downtown

The Fourth Horseman of the Recession

What if I told you that something worth over $700 billion has vanished into thin air over the last few years?

It’s not gold or a sunken treasure; it’s the value of office buildings in the United States.

This massive loss of money is the starting point for a huge problem that involves everything from the way we work to the health of the banks that lend money to your local businesses. The skylines of American cities, long seen as symbols of economic power, now hide a quiet and spreading crisis.

Gleaming towers in San Francisco, Chicago, and New York stand partially empty, their darkened windows reflecting a profound shift in our society.

This crisis represents a fundamental reordering of our economy, one that is creating a generation of ‘ghost towers’ and threatening to pull hundreds of American banks down with them.

Part I: The Great Emptiness

The problem starts with a simple, visible fact: emptiness.

Walk through any major downtown district in 2025, and you will feel it.

The lunchtime crowds are thinner, the coffee shops are quieter, and the office buildings are hollowed out.

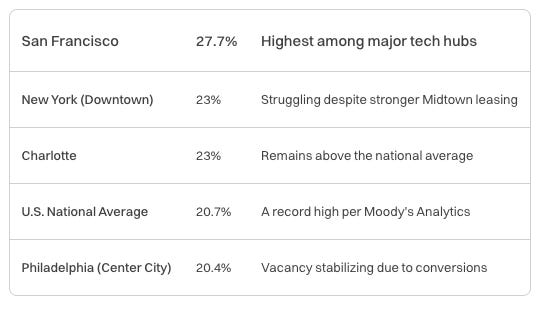

The national office vacancy rate hovers near 20%, a record high that starkly illustrates the collapse in demand for traditional workspaces.

Before the pandemic, this figure was consistently below 14%. That difference represents about 160 million square feet of office space, an enormous glut of inventory that is crushing landlords.

Even these official numbers don’t tell the full story.

They only track space that is not under lease. The reality is far worse. Many companies are still paying for offices they barely use, trapped in long-term leases signed in a different era.

With physical office attendance still down ~50% from pre-pandemic levels on any given day, a vast “shadow vacancy” exists.

As these leases expire over the next few years, the official vacancy rates are poised to climb even higher, meaning the full pain of this demand shock has yet to be felt.

This crisis is national, but its intensity is sharpest in cities that bet big on technology.

San Francisco has become the undisputed epicenter.

Its office market, once the most expensive and competitive in the world, has experienced a complete collapse.

The tech industry’s rapid embrace of remote work, combined with a wave of layoffs, has devastated the city’s commercial core, creating a cautionary tale for any economy overly dependent on a single industry.

Across the country, the story repeats in cities like Austin and Seattle, where tech-driven booms have given way to record-high vacancies.

The situation in Manhattan is more complex but reveals a crucial dynamic shaping the future of all office markets. While its overall vacancy rate is a more modest 15%, this figure masks a deep and widening split.

The market has fractured into two distinct worlds: one for the new, shiny, amenity-filled “Trophy” buildings, and another for everything else.

Companies desperate to lure employees back to the office are engaging in a “flight to quality,” competing fiercely for space in the best buildings known as Class A buildings.

Leasing for these top-tier properties in New York is now above the pre-COVID average.

At the same time, the vast majority of older, less attractive Class B and C buildings are being abandoned. They are becoming “stranded assets,” economically unviable and facing permanent obsolescence.

This growing gap is the single most important trend in the market. It shows that while the office is not dead, a huge portion of America’s existing office stock is effectively dying.

The emptiness in these towers creates a devastating ripple effect that extends far beyond the landlords. A downtown is a complex ecosystem, and for decades, its lifeblood was the daily influx of office workers.

Now, with that flow reduced to a trickle, the ecosystem is collapsing.

In Denver, where downtown office vacancy has also surpassed 30%, over 200 restaurants closed in a single year, with owners explicitly blaming the lack of office workers.

The owner of one shuttered establishment lamented, “The staggeringly low office buildings’ occupancy is killing so many businesses.”

In Seattle, the grocery chain PCC closed its flagship downtown store, citing the “persistently lower numbers of office workers.”

This story is the same for the countless dry cleaners, gift shops, and bars that once thrived on the lunchtime and happy-hour crowds. This widespread collapse of small businesses erodes the vibrancy and safety of city centers, creating a feedback loop of decline. Fewer shops and restaurants make downtown less appealing, leading even more people to stay away.

This decline strikes directly at city finances.

Less foot traffic means less sales tax collection.

More importantly, as office building values plummet, so does the property tax revenue they generate, which is often the single largest source of income for a municipality. Cities like San Francisco and Chicago are facing significant budget shortfalls as their commercial tax base evaporates, forcing them to consider cutting essential services like public transportation, sanitation, and safety.

The very systems that make a city run are being starved of the resources they need to function, all because the buildings at their core have gone quiet.

Part II: The Financial Time Bomb

This physical crisis of emptiness has triggered a brutal financial crisis of devaluation. The stunning lack of tenants has erased an estimated $740 billion in asset value since 2019, with the average sale price of an office building plummeting by 37%.

In the central business districts of major cities, the collapse has been even more severe, with prices down a staggering 60%.

This massive loss in value transcends a mere paper loss, functioning instead as a direct assault on the collateral that underpins trillions of dollars in loans.

Recent transactions show the carnage in real time: in Los Angeles, the 62-story Aon Center, a landmark tower, sold at a 45% discount to its last sale price.

To understand why this is happening, you need to know about a simple concept called a “cap rate.”

Think of it as the expected yearly return on a real estate investment.

If you buy a building for $10 million and it generates $500,000 in annual profit (after expenses), your cap rate is 5%.

For years, when interest rates were near zero, investors were happy with low cap rates of 4% or 5% because it was still a better return than they could get from a safe government bond.

But now, with interest rates much higher, investors demand a better return to justify the risk of owning a building.

They might demand a 7% or 8% cap rate.

For the building’s profit to equal an 8% return, its price must fall dramatically.

The same $500,000 in profit at an 8% cap rate means the building is now only worth about $6.25 million.

The value of the building fell by nearly 40% without a single tenant leaving, simply because the cost of money went up.

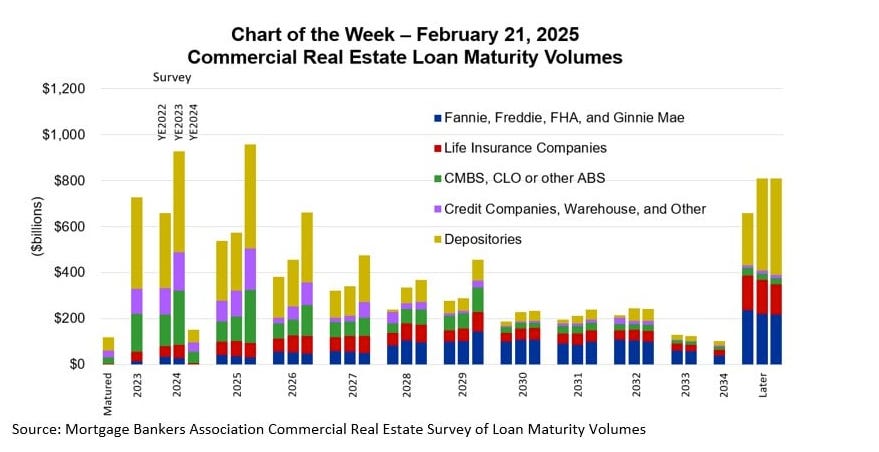

Compounding this value destruction is a financial time bomb: the “maturity wall.”

In 2025 alone, an unprecedented $957 billion in commercial real estate loans are coming due.

This figure is nearly three times the historical average.

The wave continues into the following years, with over half a trillion dollars in loans maturing in both 2026 and 2027.

The office sector, the most troubled part of the market, is the most exposed.

Roughly a quarter of all outstanding office loans must be refinanced this year.

This presents an impossible challenge for building owners, creating what is known as the “refinancing gap.”

Let’s walk through a concrete example.

Imagine a company bought an office building in 2017 for $100 million.

They put down $25 million of their own money and took out a $75 million loan.

Now, in 2025, that loan is due.

But because of high vacancy and higher interest rates, the building is now only valued at $60 million.

A bank today will only lend about 60% of a building’s value, so the best new loan the owner can get is $36 million ($60 million x 0.6).

To pay off the original $75 million loan, the owner needs to come up with the $39 million difference in cash.

They are being asked to pour more new money into the building than their entire original investment, all while the property is losing money.

For the vast majority of owners, this is impossible.

This is the financial trap that is snapping shut on landlords across the country, leaving them only two choices: default and surrender the property, or beg the bank for another short-term extension in the desperate hope that things will magically improve.

The stress is most visible in the Commercial Mortgage-Backed Securities (CMBS) market, where riskier loans are packaged and sold to investors.

This market acts as a canary in the coal mine, and right now, it is signaling extreme danger.

The delinquency rate for office loans within CMBS pools has surged to a historic high.

Even more alarming, of the office loans scheduled to mature before the end of 2026, the majority have already been transferred to “special servicing,” a designation for loans on the brink of default.

The canary is no longer singing.

Part III: Anatomy of a Perfect Storm

The current situation is the result of a perfect storm, the collision of two massive, independent forces that created a vicious, self-reinforcing cycle of decline.

The first was the structural shock of remote work.

The pandemic permanently changed our relationship with the office.

It is no longer the default place for individual work; it is now a destination for collaboration and culture-building.

The second force was the financial shock from the end of cheap money.

The loans now coming due were secured when interest rates were at historic lows, often between 3% and 4%.

Today, after the Federal Reserve’s aggressive fight against inflation, those same loans would be priced between 5% and 10%, with some short-term financing exceeding 12%.

This means an owner’s debt payments could easily double overnight upon refinancing.

The era of “higher for longer” interest rates has created a harsh new reality for a debt-dependent industry.

These two shocks have created a powerful negative feedback loop.

It works like this:

Remote work reduces demand, which lowers a landlord’s rental income.

That lower income leads to a lower property valuation.

When the owner tries to refinance this less valuable building at a much higher interest rate, the numbers no longer work.

Lenders have strict rules about how much income a property must generate relative to its mortgage payment.

With lower income and a higher required payment, the property fails the bank’s test.

Unable to secure a new loan, the owner is forced to sell at a fire-sale price or default.

That distressed sale then becomes a new “comparable” for appraisers, who use it to mark down the value of all the surrounding buildings, making it harder for their owners to refinance.

This is the vicious cycle that is systematically gutting the market.

This crisis is fundamentally different from the last major real estate crash in 2008. The 2008 crisis was primarily a residential housing disaster fueled by reckless and fraudulent lending practices.

It was a financial crisis that caused a temporary collapse in demand.

When the financial system was stabilized, demand eventually returned, and the market recovered.

Today’s crisis is the inverse.

It is not driven by bad loans, but by a permanent, structural collapse in demand for a specific type of asset: the office.

The lending standards for these buildings were generally sound when the loans were made.

The problem is that the world changed in a way that no one’s financial model predicted.

This makes the current crisis potentially more difficult to solve.

In 2008, the government could bail out the banks to fix the financial plumbing.

Today, the government cannot force companies to use office space they no longer need.

Unlike a temporary slump that would fix itself, this crisis is a deep and lasting change in the value of office buildings

Part IV: The Contagion to Main Street

While the crisis started in office towers, its greatest danger lies in its potential to spread to Main Street.

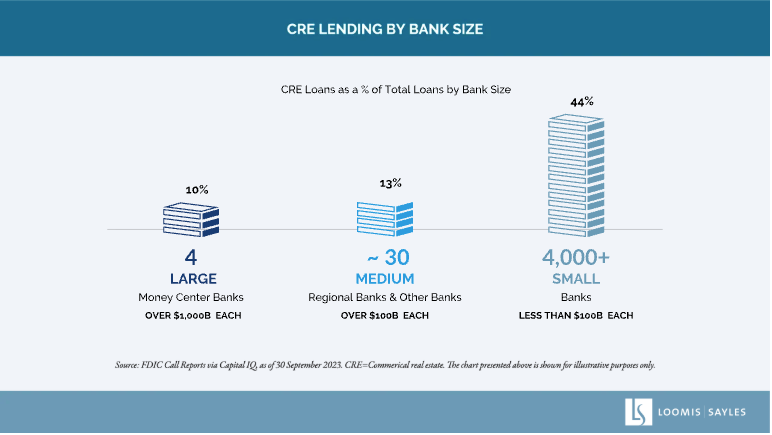

The risk is dangerously concentrated in the nation’s small and mid-sized regional banks.

These institutions are the primary lenders to local businesses across America, and their balance sheets are saturated with commercial real estate loans.

CRE loans make up an average of 44% of total loans at these banks, compared to just 13% at the giant “too big to fail” banks.

In fact, smaller banks hold over two-thirds of all CRE debt in the country.

This concentration is a ticking time bomb.

This risk was effectively shifted from the big, heavily regulated banks to the smaller ones over the past decade. After the 2008 financial crisis, new regulations made it harder for the largest banks to make these kinds of loans, so regional banks eagerly stepped in to fill the void.

Now, the bill for that decade of aggressive lending is coming due.

A wave of office loan defaults could wipe out the capital of hundreds of these smaller institutions, rendering them insolvent.

The failure of even a few could spark a crisis of confidence, leading to the kind of deposit runs that toppled Silicon Valley Bank and Signature Bank in 2023.

The economic damage would spread quickly.

A weakened regional banking sector would be forced to pull back on lending, creating a credit crunch that would starve small and medium-sized businesses of the capital they need to grow and create jobs.

In this way, the fate of a half-empty skyscraper in downtown Los Angeles is directly connected to the health of the broader American economy.

Part V: Wreckage and Opportunity

Faced with this grim reality, many have pointed to a seemingly obvious solution: convert the empty office buildings into apartments.

While this is a promising idea that will certainly be part of the long-term answer, it is not a simple fix.

The biggest obstacle is physical.

Most office buildings, especially those built in the latter half of the 20th century, have very deep “floor plates.”

This means the distance from the central elevator core to the windows on the perimeter is vast.

This design is efficient for packing in cubicles, but it is terrible for creating livable apartments.

It results in long, dark, windowless spaces that are unsuitable for bedrooms or living rooms.

Converting these buildings often requires massive architectural interventions, like cutting large atriums through the center of the structure, which is incredibly expensive and complex.

The financial and logistical hurdles mean that conversion is only a viable option for a small fraction of the vacant office stock.

The path to stability will be a long and painful process of price discovery.

The market is not expected to find a bottom for at least another year or two as the wave of maturing debt forces the sale of distressed assets.

When recovery does come, it will be defined by the great divide.

The premium, trophy assets will stabilize first, but the vast majority of older buildings will face a grim future of deep discount sales, conversion, or demolition.

For well-funded investors who have been waiting on the sidelines, this separation will create what many are calling a “generational opportunity” to acquire properties at a fraction of their replacement cost.

Part VI: The Future of the American Downtown

This crisis is forcing a necessary and overdue conversation about the very purpose of a downtown.

For most of the last century, the American downtown was a place people commuted to for work, and then promptly left at 5 p.m.

The pandemic and the subsequent rise of remote work shattered that model, perhaps for good.

The challenge now is not to figure out how to refill the old office buildings, but to imagine what our cities can become in their absence.

The future of the successful American downtown is not as a dedicated office park, but as a vibrant, mixed-use neighborhood that is active 24/7.

This means embracing a mix of uses.

Some of those obsolete office towers will need to be torn down.

Others will be converted, not just to housing, but to vertical farms, college campuses, life-science labs, and data centers.

Cities will need to change zoning laws to allow for this flexibility and provide incentives for these difficult and expensive redevelopment projects.

The ground floors will need to be reactivated with the kind of unique retail, restaurants, and cultural venues that make a place worth visiting.

The streets themselves will need to be redesigned to prioritize people over cars, with more green space, public plazas, and bike lanes.

This transformation will be incredibly difficult and will take decades.

But the crisis of the ghost towers presents a once-in-a-generation opportunity to correct the mistakes of the past.

It is a chance to move away from the sterile, nine-to-five business districts and build more resilient and interesting downtowns.

The challenge now is to sort through the pieces and build something entirely new, with a stronger foundation that doesn’t depend on everyone being in an office five days a week.

This is the fourth piece in a four-part series on the ‘Four Economic Horsemen of the Apocalypse’ focused on the systemic risks facing the US and Global Economy in 2025.