The Most Dangerous Loan in America Is Probably in Your Driveway

The First Horseman of the Recession

If I asked you to name a risky financial product, you’d probably think of something from Wall Street. Complicated derivatives, cryptocurrency, junk bonds. You likely wouldn't think of the loan you used to buy your Honda CR-V.

But I think a strong case can be made that for millions of Americans, the most dangerous debt they hold is for the car sitting in their driveway. It’s a problem hiding in plain sight.

We see our cars every day.

We need them to live our lives.

They feel normal, safe, and essential.

The loans we used to buy them, however, are becoming anything but safe. A strange combination of events over the last few years has turned the humble auto loan into a quiet crisis.

The Recipe for Disaster

No single decision created this mess.

It was three forces coming together to create a new crisis.

The first was the Great Car Price Panic.

It started around 2021.

Hopefully, you remember it.

A global shortage of computer chips meant automakers couldn't build enough new cars. Suddenly, dealership lots were ghost towns. This scarcity created a frenzy. Used cars, once a predictable and affordable option, became hot commodities. Prices for used vehicles shot up an unbelievable 34% from 2019 levels. New cars jumped over 21%. The scarcity of cars on dealer lots kicked off a full-blown panic among buyers.

We were all told that if we didn't buy a car right now, we might be priced out forever. So, we did what seemed logical. We paid the inflated prices, and to do that, we took on bigger loans than ever before. That was the foundation of the problem: millions of us borrowing record amounts of money for an asset whose value was temporarily, and artificially, sky-high.

Then came the second ingredient: soaring interest rates. Just as we were signing these massive loans, the Federal Reserve began aggressively raising interest rates to fight inflation. Auto loan rates, which had been low for years, suddenly doubled. An average used car loan jumped to nearly 15%.

Think about what this did.

It hit families with a brutal one-two punch.

First, the price of the car was inflated. Second, the cost to borrow money for that car was also inflated. This sent the average monthly car payment soaring past $700. For borrowers with weaker credit, the rates were often far worse, making their payments almost impossible to manage.

An average used car loan jumped to nearly 15%

The final ingredient was the removal of the financial safety net.

During the pandemic, stimulus checks and expanded benefits had helped keep many families afloat. But over the last few years those programs have ended. That extra cushion disappeared right at the moment when household budgets were being squeezed by inflation on everything from groceries to rent. Families were left walking a financial tightrope with no net, just as their car payments turned into a massive problem.

The Bill Comes Due

For a while, the problem was mostly invisible.

But now, the bill is coming due, and the numbers are starting to paint a grim picture.

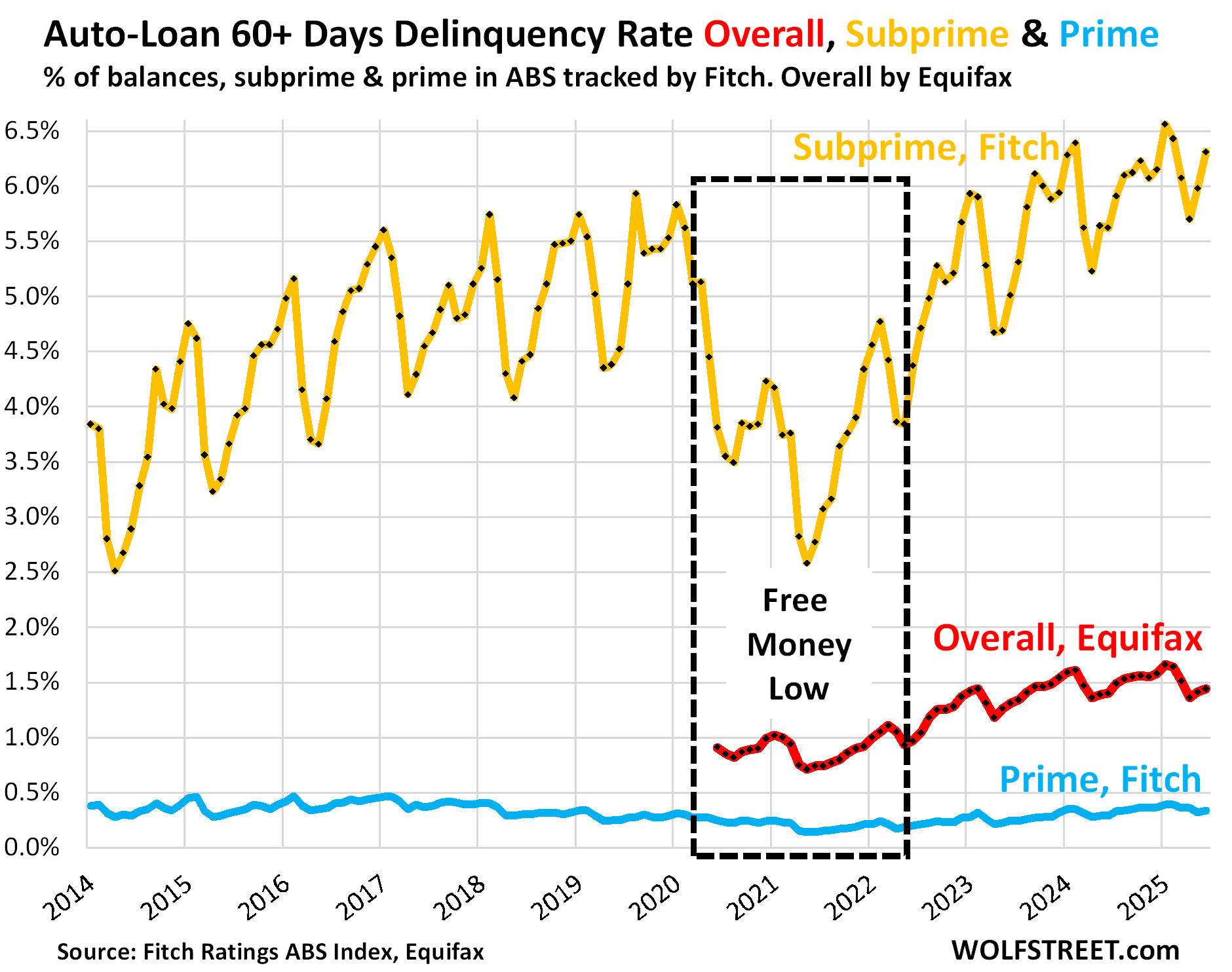

The most alarming signs are coming from what banks call "subprime" borrowers, meaning people with lower credit scores who often have the least financial breathing room. Today, over 6% of these borrowers are more than 60 days behind on their car payments.

That is the highest number ever recorded.

Let me put that in perspective. The amount of subprime auto borrowers seriously behind on their car payments has now officially surpassed the peak of the 2008-2009 Great Recession. This means the financial stress on the average car owner is worse today than it was during one of the biggest economic crises in American history.

This wave of missed payments has a brutal, real-world outcome: repossession.

Last year, an estimated 1.73 million vehicles were repossessed, the highest number since 2009. That’s millions of families who walked outside one morning to find an empty space where their car used to be. In a country where you need a car for almost everything, from getting to work to buying groceries, losing a vehicle can send a family’s life into a downward spiral.

The System Starts to Seize Up

When this many people stop paying their loans, the entire system starts to feel the pressure. Lenders who were handing out loans freely just a couple of years ago are now getting spooked. They are looking at their losses piling up and are hitting the brakes.

This leads to a credit crunch.

Banks are tightening their standards, making it much harder to get a loan. Rejection rates for auto loans are at an all-time high creating a new trap. The very people who need a car to improve their financial situation are now the ones being locked out of the market. It also hurts the automakers and the economy as a whole, because if people can't get loans, they can't buy cars.

And this isn't just happening in the United States.

In places like Thailand, a similar story is playing out. High household debt and falling used car values have led to a spike in defaults. Throw in the preference for cheap Chinese EVs over legacy gasoline cars and the problem only gets worse.

In response, Thai banks have become so strict that they are reportedly rejecting up to 70% of loan applications in some areas. This has caused their car market to slump to a 15-year low.

It’s a warning sign that this isn't a uniquely American problem, but a global vulnerability.

What Happens Next?

We are at a strange and precarious moment. The panic-driven decisions of the last few years have created a massive, indigestible lump of bad debt in the auto market. Millions of people are "underwater," owing much more on their cars than they are actually worth, trapping them in unaffordable payments with no easy way out.

The real question is whether this fire can be contained or if it's about to jump to other parts of the economy. For now, the damage is mostly concentrated on car owners and the lenders who serve them. But what happens if a softening job market pushes even more people over the edge?

The car in your driveway used to be a symbol of freedom and opportunity.

But for a growing number of Americans, it has become a symbol of financial ruin.

This is the first piece in a four-part series on the 'Four Economic Horsemen of the Apocalypse' focused on the systemic risks facing the US and Global Economy in 2025.