The Math Just Doesn’t Math

America’s Quiet Debt Crisis

There's a moment every month that millions of Americans dread. It’s when they sit down at the kitchen table, the house finally quiet, and spread out the bills under the stark cone of a single light. It’s a private, stressful ritual.

On one side is the paycheck, or what’s left of it after taxes. On the other is a merciless list of demands:

Mortgage or rent

Car payments

High utility bills

Groceries

Childcare

All wrapped up in a white envelope from hell, the credit card statement.

Their balances grow with a quiet, relentless force.

In this moment, the math just doesn't add up.

The numbers refuse to align.

It’s a feeling of falling, a knot in the stomach that tightens with every dollar of interest. To get through the month, a choice has to be made.

It's not between a want and a need, but between one necessity and another. The card is swiped for gas to get to work, for prescriptions, or for a child’s shoes, all with the silent prayer that next month will be different.

But it rarely is.

This scene, happening in countless homes across the country, is the real, untold story of the U.S. economy in late 2025. While economic headlines may point to resilient GDP growth and a stable job market, they paint a dangerously incomplete picture.

They hide the slow-burning crisis of debt that has pushed a huge part of the American population to the financial edge.

The End of the Cushion

It feels like a lifetime ago, but it wasn't.

In 2021 and early 2022, many American families felt a sense of security they hadn’t experienced in years. A combination of government stimulus, enhanced unemployment benefits, and reduced spending during lockdowns had allowed households to accumulate an astonishing $2.1 trillion in "excess savings."

For the first time in a generation, millions of people had a buffer. If the car broke down or a child got sick, it was a problem, not a catastrophe. It was the feeling of being able to breathe.

But that breathing room was short-lived. As the world reopened, a new economic force took hold: the most aggressive inflation in forty years. At first, it was a distant headline, a concern for economists. Then, it arrived at the gas pump and the grocery aisle.

A gallon of milk ticked up by a dollar.

A tank of gas that used to cost $40 now cost $60.

Then the weekly grocery bill swelled from $250 to $350 without a single luxury item in the cart.

This was inflation’s true corrosive effect.

Inflation acted like a silent tax, draining money from every family’s budget. The bathtub full of savings now had its drain pulled wide open. For about 80% of American households, which includes not just the poor but the vast middle class, that savings cushion wasn't just reduced. It was wiped out. By 2024, according to the San Francisco Fed, the aggregate savings for the country had tipped into the negative, meaning we had spent all the buffer and then some.

The experience, however, was not shared equally.

The experience was not shared equally. The wealthiest 20% of households still held on to a large financial reserve.

For everyone else, the shock absorber was gone.

The car of the household economy was now driving on a bumpy road with no suspension, and every pothole was felt with a jarring, bone-rattling thud.

The Great Re-Leveraging

When the savings ran out, something had to take their place. For millions, that replacement was high-interest credit card debt. The credit card, once a tool for convenience, became the new, terrifyingly fragile safety net. People weren't racking up debt on designer clothes. They were going into debt buying eggs, bread, and medicine. This was debt for survival.

The numbers are staggering. As of mid-2025, total U.S. household debt stands at a record $18.39 trillion. But the most telling figure, the one that speaks to the immediate pressure on families, is the $1.21 trillion in outstanding credit card debt. This is an all-time high, a mountain of the most expensive and unforgiving kind of debt, growing at a rate of nearly 6% year-over-year.

This creates a brutal mathematical problem.

Carrying a balance is like trying to run up a down escalator. You can make your minimum payment every month, pouring hundreds of dollars toward your debt, only to watch the balance barely move as punishing interest charges pile right back on.

In the years after the 2008 crisis, households deleveraged, paying down mortgages. A mortgage, for all its burdens, is typically "good debt", in that it is used to acquire an asset that, one hopes, will appreciate in value and build family wealth.

The debt being accumulated today is the opposite.

It is unsecured, high-interest debt used for consumption.

It doesn't build a future; it mortgages it.

This story plays out differently across demographics, but the theme is the same. Consider a young family, already saddled with student loans from a decade ago. Now, they face childcare costs that rival a mortgage payment.

When their son needs an unexpected trip to the emergency room, the $2,000 bill goes on a Visa because their savings are gone.

Or think of the gig worker, whose income fluctuates wildly from month to month. They use credit cards to smooth out the gaps, paying for groceries in a lean week with the hope of paying it off in a good one.

But a few bad weeks in a row, and the balance spirals out of control.

Even retirees on fixed incomes are not immune. Their pensions and Social Security checks don't keep pace with the rising cost of prescriptions and property taxes, forcing them to put essential medical care on a MasterCard.

These are not stories of irresponsible people. They are stories of ordinary Americans trapped in an economic vise.

The Cracks Begin to Show

For a while, this debt-fueled consumption can hide the dangers hiding underneath. But a system built on such shaky foundation cannot hold forever. Now, in late 2025, the cracks are beginning to show. The clearest signs of distress are the rising numbers of people who are failing to pay their bills.

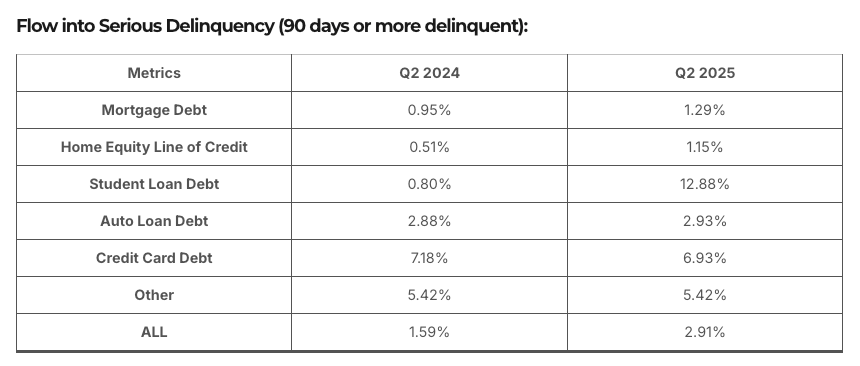

The data from the Federal Reserve is a clear warning. The amount of credit card debt that is "seriously delinquent," meaning 90 or more days past due, is at its highest level in over a decade, 6.93%. This means that for every $100 owed, about $7 is now severely behind.

It’s a signal that a growing number of people have hit their breaking point.

They have nothing left.

Perhaps the most dramatic shock is the surge in student loan defaults. After a long pause, repayments have resumed. The consequences were immediate. An astonishing 12.88% of student loan balances are now seriously delinquent. This has created a massive new source of financial pain for millions, damaging their credit scores for years to come.

Delinquency isn't just a statistic. It’s a deeply personal and often shameful experience. It means the start of relentless calls from debt collectors. It means watching your credit score plummet, which slams the door on future opportunities.

It is a financial scar that doesn't easily heal.

The distress is particularly acute among younger Americans, those under 40, who are facing delinquency rates not seen since the immediate aftermath of the Great Recession.

They are the canary in the economic coal mine, and they are struggling for air.

The Tale of Two Economies

This raises a confusing question. If things are so bad for so many, why does overall consumer spending still seem strong? The answer is that we are living in a tale of two consumers.

High-income households have mostly weathered the storm. They hold the bulk of the remaining savings and benefit from a strong stock market. Their spending has remained healthy. Because they spend so much more than everyone else, their activity keeps the national averages afloat. Their ability to buy luxury goods and travel masks the deep cuts happening everywhere else.

This creates a major risk. Policymakers may look at the top-line numbers and conclude that everything is fine.

But this is like judging the health of a forest by only looking at its tallest trees while ignoring the decay on the forest floor.

The reality is that lower and middle-income households are cutting back. They are switching to cheaper grocery brands, canceling subscriptions, and putting off necessary repairs. This two-track economy is fragile. It relies entirely on the spending of the wealthy.

If a stock market shock caused them to pull back, there would be no one left to pick up the slack. The broad base of consumers has no more savings and no more room on their credit cards.

The final option for those with nowhere else to turn is bankruptcy. After years of historic lows, personal bankruptcy filings are now climbing by nearly 12% a year. This is the final, desperate admission that the math will never work again.

A Nation Weighed Down

Behind these trillions of dollars in debt are millions of human stories: families choosing between paying a credit card bill or a utility bill, young people whose student loan debt prevents them from ever dreaming of buying a home, and parents using high-interest plastic to put food on the table.

These people are the bedrock of the country. Their growing financial problems are a direct threat not just to the economy, but to the promise of a secure American middle class.

The current trajectory is unsustainable.

The current path cannot be sustained.

An economy cannot succeed when its foundation is being hollowed out by debt. The flashing red lights on the consumer dashboard are not minor glitches.

They are symptoms of a deep crisis.

We are witnessing the slow-motion exhaustion of the American consumer, and we can no longer afford to look away.

This is the second piece in a four-part series on the 'Four Economic Horsemen of the Apocalypse' focused on the systemic risks facing the US and Global Economy in 2025.