The Japanese Widowmaker

For decades, betting against Japan destroyed careers. Now, betting on Japan might destroy the financial system.

On Wall Street, there should be a graveyard for careers destroyed by the “Widowmaker”

For decades, this was the nickname given to a specific bet: betting that the Bank of Japan would finally run out of money or patience. Traders would look at Japan’s massive debt and say, “This can’t last. Interest rates have to go up.”

They would bet millions that the Japanese bond market would crash.

But year after year, the Bank of Japan refused to blink.

They printed more money

They bought more bonds

They kept rates at zero.

The traders lost everything.

The Bank of Japan always won.

It became an iron law of finance: Never bet against Japan’s ability to keep things exactly the same.

But while the Widowmaker trade destroyed those who bet against Japan, another trade was making billions for those who bet with Japan.

It was a strategy based on a simple, irresistible idea: the “Free Lunch.”

The setup was almost too good to be true. You could borrow money in Japan for basically free, zero percent interest. Then, you could take that money and invest it anywhere else in the world where interest rates were higher, like the United States or Australia.

You pocketed the difference, and you didn’t have to do any real work.

This was the “Yen Carry Trade.”

For twenty years, this trade was the engine of global finance. It felt like a magic money machine.

But now, the machine is breaking.

The Bank of Japan is finally running out of road, and the “Free Lunch” is over.

The Widowmaker has flipped.

The dangerous bet is no longer betting that Japan will change; the dangerous bet is assuming Japan can stay the same.

We are watching the end of an era. The unwinding of this massive trade is not just a problem for Tokyo.

It is a trap that has snagged the entire global economy.

The Origins of the Zero-Cost World

To understand why this is happening, you have to look back at how Japan became the world’s strangest bank.

In the 1990s, Japan was the future.

Then, its massive economic bubble burst. Property prices crashed, the stock market collapsed, and the country fell into a deep hole of “deflation.”

Deflation is when prices keep falling.

That might sound nice when you are buying groceries, but for an economy, it is a disaster.

When prices fall, businesses make less money.

When they make less money, they cut wages.

When wages drop, people spend less, and prices fall even further.

It is a death spiral.

Japan spent decades trying to break out of this spiral. They tried everything.

They built bridges to nowhere to create jobs. They handed out cash. But nothing worked. So, the Bank of Japan (the BOJ) decided to do something radical. They decided to make money free.

In 1999, they cut interest rates to zero. This was the birth of the “Zero Interest Rate Policy,” or ZIRP. It was supposed to be an emergency measure, but the emergency never ended.

Japan kept rates at zero for so long that an entire generation of traders grew up thinking it was normal.

When zero wasn’t enough, they went even further. In 2016, they introduced “Negative Interest Rate Policy,” or NIRP. This meant that if a bank wanted to park its extra cash at the central bank, it had to pay a fee. They were effectively charging people to save money. The goal was to force that money out into the economy.

Then came “Yield Curve Control,” or YCC. The BOJ promised to buy as many government bonds as necessary to keep long-term interest rates low.

They were printing Yen to buy their own debt, keeping the cost of borrowing artificially cheap.

Japan became an outlier.

While the rest of the world eventually started raising rates, Japan stayed at the bottom. This created a massive gap.

If you could borrow in Yen at 0% and lend in U.S. Dollars at 5%, you made a 5% profit for doing nothing.

This gap is what fueled the Carry Trade. It wasn’t just hedge funds doing it.

Japanese families, pension funds, and insurance companies were all doing it.

They took their savings out of Japan, where it earned nothing, and sent it overseas. Japan became the world’s largest creditor, with over $3 trillion invested abroad.

The world got addicted to this flow of cash. Japanese money bought U.S. government bonds, keeping American mortgage rates low.

It bought Australian mining stocks.

It bought Brazilian debt.

It was a constant stream of cheap liquidity that greased the gears of the global financial system.

Everyone assumed the Free Lunch would last forever. But in economics, things that can’t go on forever eventually stop.

The Mystery of the Missing Inflation

You might be asking two questions here.

First, how did Japan rack up so much debt?

And second, if they printed trillions of Yen for twenty years, why didn’t prices skyrocket immediately?

The answer to both lies in the trauma of the crash.

When Japan’s bubble burst in the 1990s, it wiped out the wealth of an entire generation. Companies and families were terrified. They stopped spending and started saving every penny.

This created a rare economic phenomenon called a “Liquidity Trap.” Even though the Bank of Japan printed money and made borrowing free, people refused to borrow.

They didn’t trust the future.

The money didn’t circulate in the economy to buy cars or houses; it just sat in bank vaults.

Because the money wasn’t chasing goods, prices didn’t go up.

To keep the economy from freezing to death, the government had to step in.

Since the private sector wouldn’t spend, the government spent money for them.

They built bridges, tunnels, and roads just to keep people employed. They did this year after year for three decades.

This kept the economy on life support, but it came at a massive cost. The government racked up a credit card bill worth 2.5 times the size of their entire economy. They essentially mortgaged their future to survive the present.

The Wrong Kind of Inflation

The crack in the system appeared from an unexpected direction: inflation.

For thirty years, Japan desperately wanted inflation. They wanted prices to go up just a little bit, to prove their economy was alive. In 2022, they finally got their wish. But it wasn’t the good kind of inflation.

Good inflation comes when people have great jobs, get raises, and spend more money. That pushes prices up because demand is strong.

Japan got the bad kind: “Supply-Push Inflation.”

This happens when the staples you need to buy: oil, gas, and food, get more expensive. Japan imports almost all its energy and a lot of its food. When energy prices spiked globally, Japan had to pay the bill.

But there was a multiplier effect. Because the Bank of Japan refused to raise interest rates while the United States was raising them aggressively, the Yen crashed.

In finance, money flows to where it is treated best.

If the U.S. pays 5% interest and Japan pays 0%, investors sell Yen and buy Dollars.

The selling was relentless. The Yen, which used to trade around 100 to the dollar, weakened to 130, then 140, then 150. At one point, it flirted with 160.

This crushed the Japanese people. A weak Yen makes everything Japan buys from abroad more expensive. The price of gasoline surged. The cost of bread and milk went up. Real wages, the amount you can actually buy with your paycheck, fell for over two years straight.

The Japanese public was furious. The government’s approval ratings tanked. The “weak Yen” policy, which was supposed to help big exporters like Toyota sell cars, was hurting regular families.

The government tried to intervene. They spent billions of dollars buying their own currency to prop it up. It was like trying to stop a waterfall with a bucket.

As long as the interest rates remained zero, the market knew the Yen was weak.

This created a political crisis. The Bank of Japan realized it could no longer ignore the problem. The Free Lunch was becoming too expensive for Japanese voters to bear.

They had to start closing the gap.

They had to start raising rates.

The Pivot to Tourism

In the middle of this crisis, Japan found one unexpected lifeline: tourists.

Because the Yen was so weak, Japan became the cheapest travel destination in the developed world. A bowl of ramen that used to cost $10 in dollar terms now cost $6. A luxury hotel room in Tokyo was suddenly half the price of a similar room in New York or London.

The world noticed. Tourists flooded into the country. Kyoto became so crowded that locals couldn’t get on public buses. Tokyo’s streets packed with visitors buying luxury bags, electronics, and sushi.

The government leaned into this hard. They saw tourism as a way to bring foreign money directly into the local economy. If they couldn’t export cars as easily, they would export “experiences.” They set ambitious goals to double the number of visitors and the amount of money they spent.

But tourism is a double-edged sword. While it brought in cash, it also drove up prices for locals even more. Hotels became too expensive for Japanese travelers. Restaurants raised prices to match the tourists’ wallets. It created a two-tier economy: one for the visitors with their strong dollars and euros, and one for the locals with their shrinking Yen.

More importantly, tourism isn’t enough to fix the structural rot. You cannot build a G7 economy entirely on serving noodles to backpackers. The scale of Japan’s debt and the size of its financial system are just too big. Tourism was a nice bonus, but it wasn’t a solution to the monetary trap the BOJ had built for itself.

The Unwinding: August 2024

The real danger of the Yen trade isn’t about ramen prices. It is about leverage.

The Yen Carry Trade is a leveraged trade, where you used borrowed money to make a bet. When you borrow Yen to buy U.S. stocks, you are using leverage.

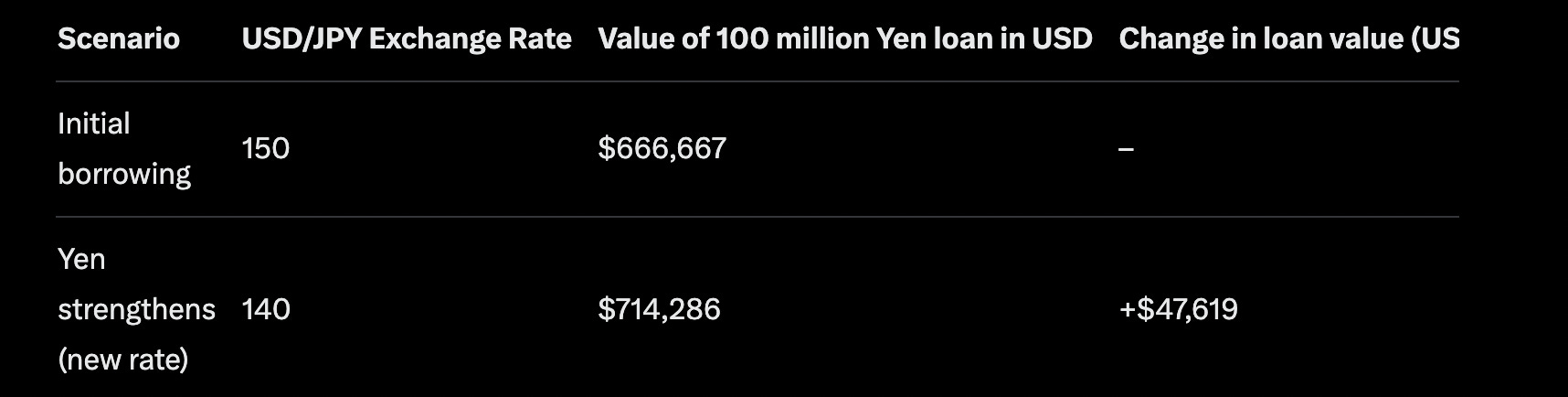

The problem with leverage is that it works great on the way up, but it kills you on the way down. If the Yen strengthens even a little bit, your loan gets bigger. If you borrowed 100 million Yen when the rate was 150, that loan was worth about $666,000. If the Yen strengthens to 140, that same 100 million Yen loan is now worth $714,000. You suddenly owe $48,000 more, or 7.14% more, just because the currency moved.

If you are a hedge fund with billions in leverage, a small move in the currency can wipe you out.

When that happens, you get a “margin call.”

The bank demands its money back immediately. To pay them, you have to sell your assets. You sell your U.S. stocks. You sell your crypto. You sell your gold.

This is exactly what happened in August 2024.

The Bank of Japan raised interest rates by a tiny amount, 0.15%.

It was a microscopic move. But it was enough to shatter the illusion that rates would stay at zero forever.

The reaction was violent. The Yen shot up in value. Traders who were shorting the Yen, betting it would go down, got crushed. They rushed for the exit all at once. To pay back their Yen loans, they had to sell everything else.

The Japanese stock market, the Nikkei, crashed 12% in a single day. It was the worst drop since 1987. But the damage didn’t stop in Japan. U.S. tech stocks plunged. Bitcoin tumbled. Markets in Europe also fell.

This event revealed how fragile the system had become. The world had built a skyscraper of risk on a foundation of cheap Yen. When the foundation shook, the whole building swayed.

Analysts estimate that hundreds of billions of dollars in carry trades were unwound in just a few weeks. But here is the scary part: many experts believe that was only the beginning. There are still massive positions out there, waiting for the next shoe to drop.

The Trap

This brings us to the present day and the impossible situation facing the Bank of Japan (BOJ). They are caught in a trap of their own making.

Option A: They continue to normalize rates.

They raise interest rates to 1% or 2% to stop the inflation that is hurting their people. The problem? The Japanese government has debt worth more than 250% of its total economy. It is the most indebted developed nation on earth.

When rates are zero, that debt is free to service. But if rates go to 2%, the interest payments on that debt would consume a huge chunk of the national budget.

The government would have to cut spending or raise taxes drastically. It could trigger a debt crisis that makes the 2008 financial crisis look small.

Option B: They give up and keep rates low. The problem? The Yen will collapse.

If the gap between U.S. and Japanese rates stays wide, the currency will slide toward 160, 170, or worse.

Import prices will soar and the Japanese people will get poorer.

The anger that is already brewing will boil over.

This is the definition of a “Lose-Lose” scenario.

If the BOJ fights for the currency, they crush the government’s finances.

If they protect the government’s finances, they destroy the currency and the people’s standard of living.

For twenty years, Japan kicked the can down the road. They used complex tricks and printed money to avoid making hard choices. But they have reached the end of the road. There is no more road left.

The decision has already been made for them by the market. The BOJ has to raise rates, slowly and painfully. The question is, can they do it without breaking the global financial system?

This is why the “Widowmaker” has flipped.

The traders who used to bet on a crash were early, but they weren’t wrong about the math.

The math eventually wins.

The anomaly of a major economy having zero interest rates for a quarter-century is correcting itself.

The Bill Comes Due

We are entering a new era of consequences. The low volatility and easy money of the 2010s were partly subsidized by Japan. It was no accident that Softbank’s Vision Fund, based in Japan, was a major contributor to the startup bubble of the 2010’s.

For the average person in America or Europe, this seems like a distant problem.

But it matters.

If Japanese investors stop buying U.S. and European bonds because they can finally get a decent return at home, interest rates in the West could stay higher for longer.

Mortgages could stay expensive.

The “easy money” that fueled tech startups and real estate booms will dry up.

The Japanese Yen was the water in the bathtub of the global economy. Now, the plug has been pulled. As the water drains out, we are going to find out just how much of our own prosperity was floating on borrowed Yen.

Japan tried to save its economy by distorting the price of money.

They managed to keep the game going longer than anyone thought possible.

But the trap has finally snapped shut.

The Bank of Japan must now choose between a debt crisis and a currency crisis, and the rest of the world has to brace for the impact.