Tesla’s $2B xAI Investment

When “What Shareholders Asked For” Means the Opposite

On November 6, 2025, Tesla shareholders voted.

About a billion said yes to a $2 billion investment in Elon Musk’s xAI startup.

About 900 million said no.

Another 470 million abstained, enough to tip the scale.

The proposal, Proposal Seven, had been brought by Stephen Hawk, a Florida shareholder with a $2,000 stake. The board’s own recommendation was neither for nor against.

Under Tesla’s rules, not voting yes counts as voting no. The proposal failed.

Seventy-one days later, the board approved it anyway.

On January 16, 2026, Tesla’s board greenlit the $2 billion investment in xAI’s Series E preferred stock, part of a $20 billion round that valued xAI at roughly $230 billion. Other investors in that round included Valor Equity Partners, Fidelity, Qatar Investment Authority, MGX, Baron Capital, NVIDIA, and Cisco.

After the board approved it, Musk posted on X: “We’re just doing what shareholders asked us to do, pretty much.”

Tesla’s CFO, Vaibhav Taneja, went further.

On the Q4 earnings call, he said: “This is literally furtherance of our master plan four.”

What were they worried about, they seemed to be asking, that you thought we wouldn’t do exactly this?

But the story didn’t end there.

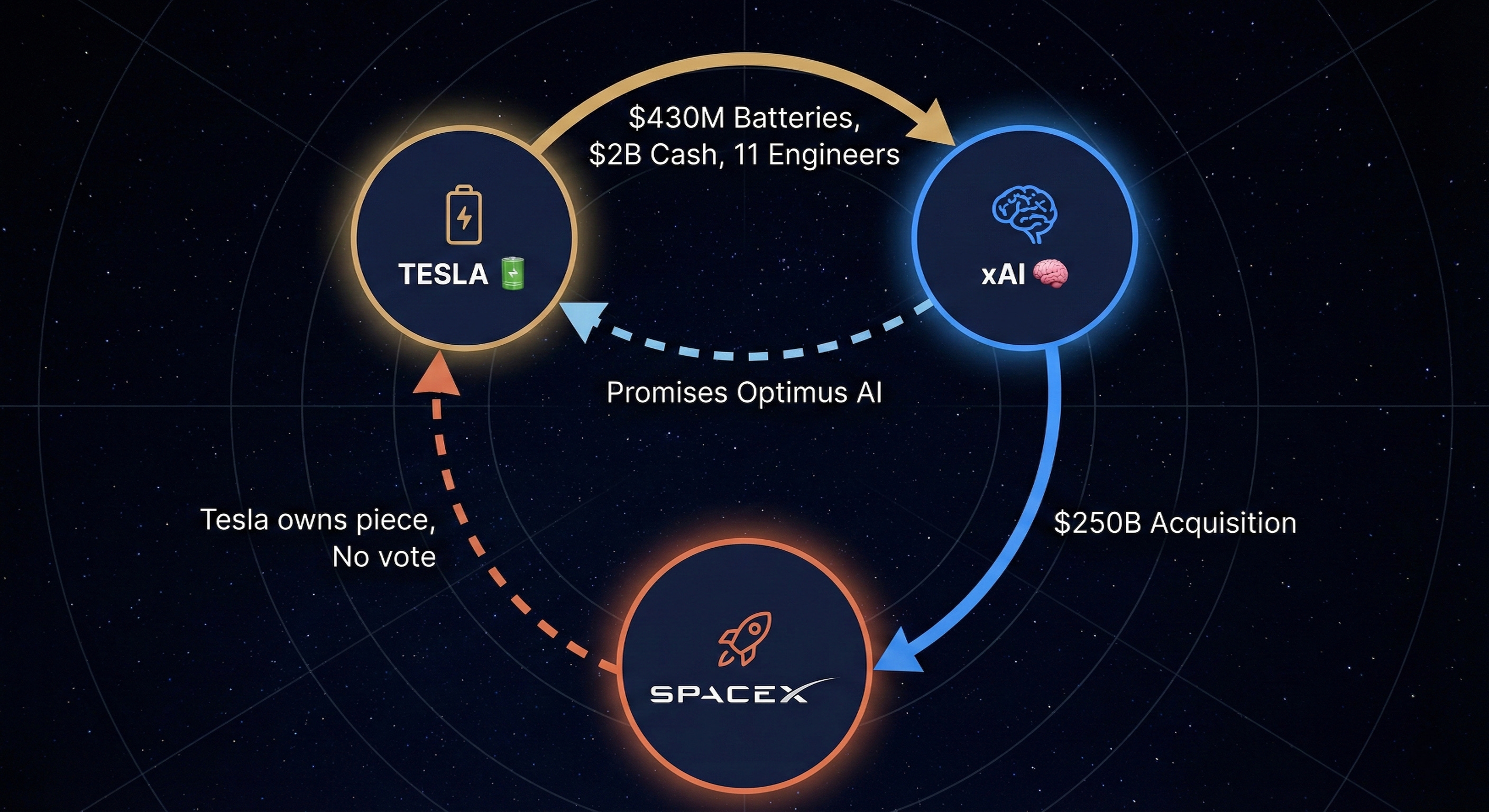

On February 2, 2026, SpaceX acquired xAI outright, creating a $1.25 trillion combined entity, the largest merger in history.

Tesla shareholders had voted against funding xAI. The board overrode them.

Three weeks later, the company they involuntarily funded was absorbed into Musk’s rocket company.

They never voted on that either.

The $2 billion itself matters less than what it represents. Venture capitalists lose money on startups all the time. The question isn’t whether xAI is a good investment.

The question is: What does a shareholder vote mean if the board can just ignore it?

Almost 47 percent of shareholders directly voted no. With the “abstains” that number is ~57% under Tesla’s rules.

The board’s position is that xAI has technology Tesla needs.

“This is literally furtherance of our master plan four” - Tesla’s CFO, Vaibhav Taneja

That argument isn’t crazy.

But a board that loses a vote and approves the same deal anyway is saying shareholder votes don’t really matter.

This is the story of how the most famous board in the world decided that your vote is just a suggestion.

The Circular Logic

To understand what happened, follow the money. It travels in a circle, and every stop belongs to Elon Musk.

Musk owns about 13% of Tesla. According to Forbes estimates, he also owned a majority stake in xAI before its January 2026 fundraise. He sits on both sides of the deal.

He did not step aside from the vote. Tesla’s 10-K says the board reviewed the deal under its related-party policy, but there was no publicly disclosed special committee to negotiate at arm’s length.

Now trace the circle.

Stop one: the hardware. In 2025, Tesla sold $430 million in Megapack batteries to xAI. These batteries power Colossus, xAI’s supercomputer. Tesla built the infrastructure xAI uses to train its AI.

Stop two: the talent. xAI recruited at least 11 engineers directly from Tesla’s AI and autopilot teams. These are not junior people. Tesla spent years and hundreds of millions training them to make self-driving work. The board could have objected. Instead, Tesla later invested $2 billion in the company that took them.

Stop three: the chips. According to the Cleveland pension fund lawsuit and Senator Warren’s letter to the SEC, over 12,000 of Tesla’s ordered Nvidia H100 chips were diverted to X and xAI. Tesla’s autonomous driving team was not the beneficiary.

Stop four: the cash. Tesla gave xAI $2 billion.

Now watch the circle close.

By January 2026, xAI was telling investors it would build AI for Optimus, Tesla’s humanoid robot. The company founded, according to shareholder lawsuits, by diverting Tesla’s resources now promises to build AI for Tesla’s robots.

Tesla paid for the hardware.

Tesla trained the engineers.

Tesla ordered the chips.

Tesla wrote the check.

And now Tesla is paying again to get access to what it already paid for.

Meanwhile, shareholders are suing, claiming xAI is “taking value from Tesla.” The company they say is draining Tesla is the company Tesla just funded.

A Tesla press release framed this as granting Tesla enhanced AI capabilities. In practice: Tesla funded a competitor, then became dependent on that competitor’s goodwill.

The merger documents revealed what was behind the curtain.

xAI was burning about $1 billion per month. It spent $9.5 billion in the first nine months of 2025 while bringing in only $210 million. Analysts called the SpaceX acquisition a rescue mission, not a strategic combination.

Tesla shareholders, overruled by the board, had invested $2 billion in a company losing money at an unsustainable rate.

The board called it “furtherance of our master plan.”

The financial statements suggest something closer to life support.

The Institutions Say No

Before the vote, both ISS and Glass Lewis recommended shareholders vote against.

These are the two biggest firms that advise pension funds and asset managers on how to vote. They don’t oppose many things. Their job is to keep shareholder voting running smoothly.

When they both recommend “no,” something is wrong.

CalPERS voted against. That’s the California public employee’s pension fund, which manages $440 billion.

They had already raised concerns about Musk’s governance. An investment officer said the deal “concentrates power in a single shareholder” and was negotiated by board members who might not be independent from the CEO.

Norway’s sovereign wealth fund, which manages $2 trillion, went further. They voted against the xAI proposal and also voted against reelecting two directors.

Both directors were reelected, but with well below average support.

Vanguard and BlackRock, which between them control roughly 10% of American equities, abstained.

Under Tesla’s bylaws, abstention counts as no.

So the two largest asset managers in the world effectively killed the vote.

They didn’t say yes. They didn’t say no.

They said “we’re not comfortable validating this.”

That was fatal.

Charles Elson, a corporate governance expert at the University of Delaware, has studied company boards for decades.

On Tesla he was direct: “I don’t think this board is capable of acting outside of Musk’s interests.”

And: “You’re essentially asking shareholders to enrich the CEO while also funding his competing business interests.”

Elson said the board showed “almost a contempt for lawful and accepted procedure.”

NYC’s pension funds sued, claiming fraud and broken promises to shareholders. Their Tesla holdings fell from $1.26 billion to $831 million, a 36 percent loss.

They own more than 3 million Tesla shares. These are real losses on money meant to pay teachers and firefighters.

Every major governance institution opposed this. ISS, Glass Lewis, CalPERS, Norway’s sovereign fund, Vanguard, BlackRock, Delaware’s top corporate governance scholar. Senators investigating. Pension funds suing.

The vote failed.

Four days ago, the investment transformed again.

Tesla’s $2 billion in xAI shares became SpaceX shares. xAI investors received 0.1433 SpaceX shares for every xAI share.

Tesla shareholders never voted on owning SpaceX. They never voted on the board’s right to swap their xAI stake for SpaceX equity.

But that’s what happened.

The abstentions that killed the proposal. The proxy advisor opposition. The pension fund lawsuits. All of it now applies to a different company than the one shareholders rejected funding.

The Information Problem

The institutions opposed it. The shareholders who voted said no. The lawsuits are multiplying.

Why doesn’t any of this seem to matter?

Because of who controls the flow of information.