Is Something Wrong in the Middle Kingdom?

When success becomes survival, and survival becomes impossible

On a Tuesday morning in July, Zeng Yuzhou stood on the edge of a high-rise in Guangzhou, looking down at a city that had once promised him everything. As the founder of Liangjiaju Building Materials, he had built an empire from China's construction boom—a home renovation chain that epitomized the country's meteoric rise. Now, with $140 million in debt crushing his dreams and over 2,000 families holding worthless prepayments, that same city stretched below him like a concrete graveyard of broken promises.

He jumped.

Four days later, Chinese social media algorithms worked overtime to bury the story, scrubbing trending topics and suppressing comments. But Zeng's death wasn't an isolated tragedy, it was part of a wave of prominent business leaders taking their own lives, each representing a different sector of China's economy, each facing the same invisible noose tightening around the necks of private entrepreneurs across the Middle Kingdom.

The Four Horsemen of Economic Despair

The pattern began on April 16, when Bi Guangjun, founder of Jindianzi Textiles, leaped from the 28th floor of a building. Insiders revealed he had invested heavily in China's new energy sector. The government had championed this industry as the future, but policy shifts and market manipulation left him stranded, watching his fortune evaporate.

On June 2, Liu Wenchao, chairman of Xizi Elevator Company, became the second casualty. His company had thrived during China's construction golden age, but as the property sector collapsed, demand for elevators vanished overnight. Chinese state media noted that Liu once said "anyone who has ambition ends up scarred", words that would prove tragically prophetic.

Then came Zeng in July 2024, followed just ten days later by Wang Linpeng in July 2025, chairman of home retail giant Easyhome New Retail Group. Wang's death was particularly telling: he died just four days after being released from police custody, highlighting how the anti-corruption apparatus had become another sword hanging over entrepreneurs' heads.

These weren't desperate small-business owners drowning in debt. These were titans of industry, leaders who had navigated China's transformation from communist backwater to manufacturing superpower. Yet something fundamental had shifted beneath their feet that made death preferable to continuing the fight.

The Perfect Storm Brewing

To understand why successful entrepreneurs are choosing death over another day in business, you have to grasp the crisis crushing China's private sector from all sides.

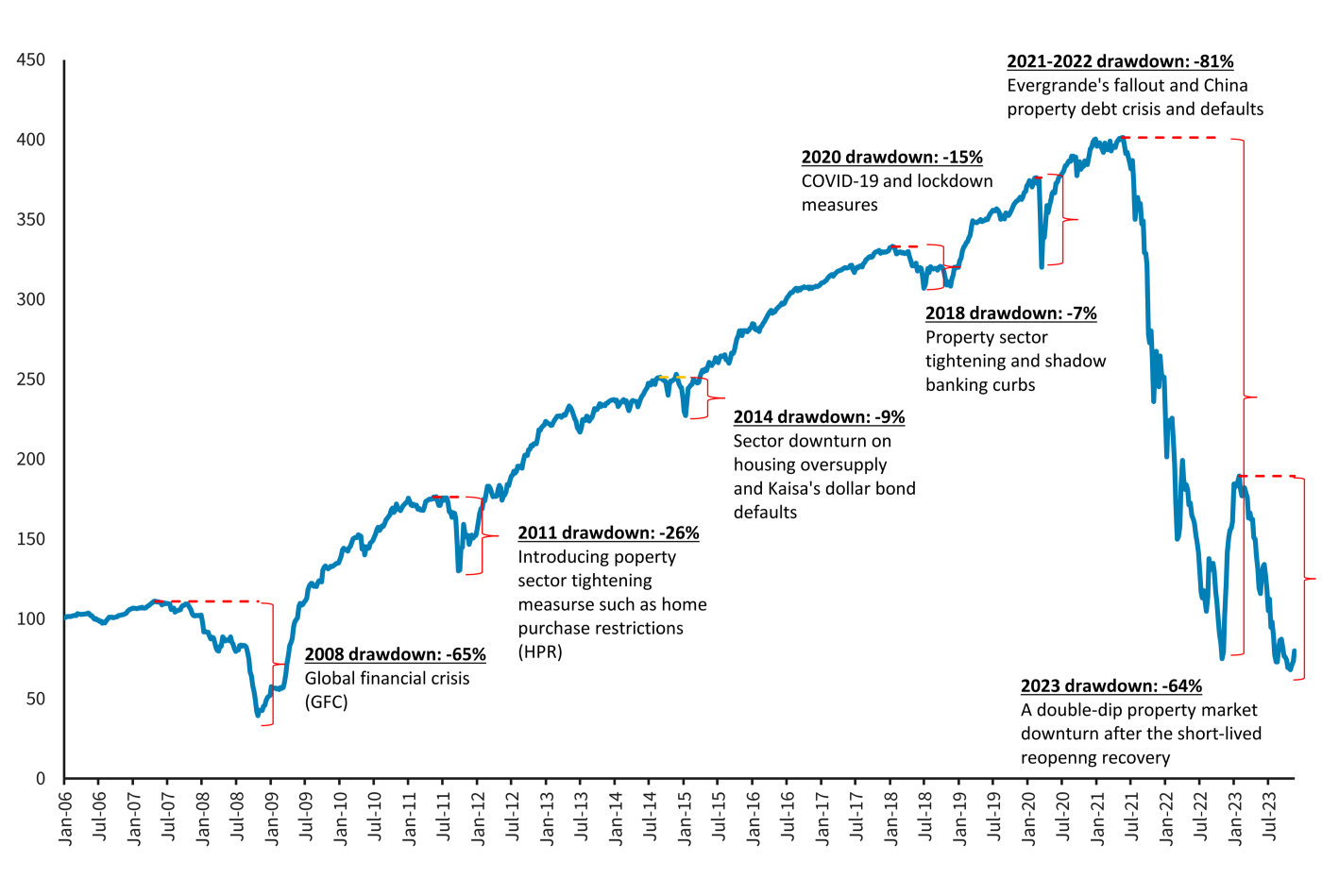

Since 2021, China's property market has been in freefall. Real estate prices registered their fastest drop in nine years during June 2024, with new home prices falling for ten consecutive months. Property investment declined 9.8% in the first four months of 2024, while new property sales plunged 28.3%.

Consider Xizi Elevator's predicament: when property developers default on payments, elevator companies don't just lose current revenue, they lose their entire business model. The construction industry that once provided predictable, growing demand simply evaporated. Meanwhile, Liangjiaju's nightmare revealed another brutal reality: customer payment cycles stretched from two weeks to six months as cash-strapped buyers and contractors struggled to stay afloat.

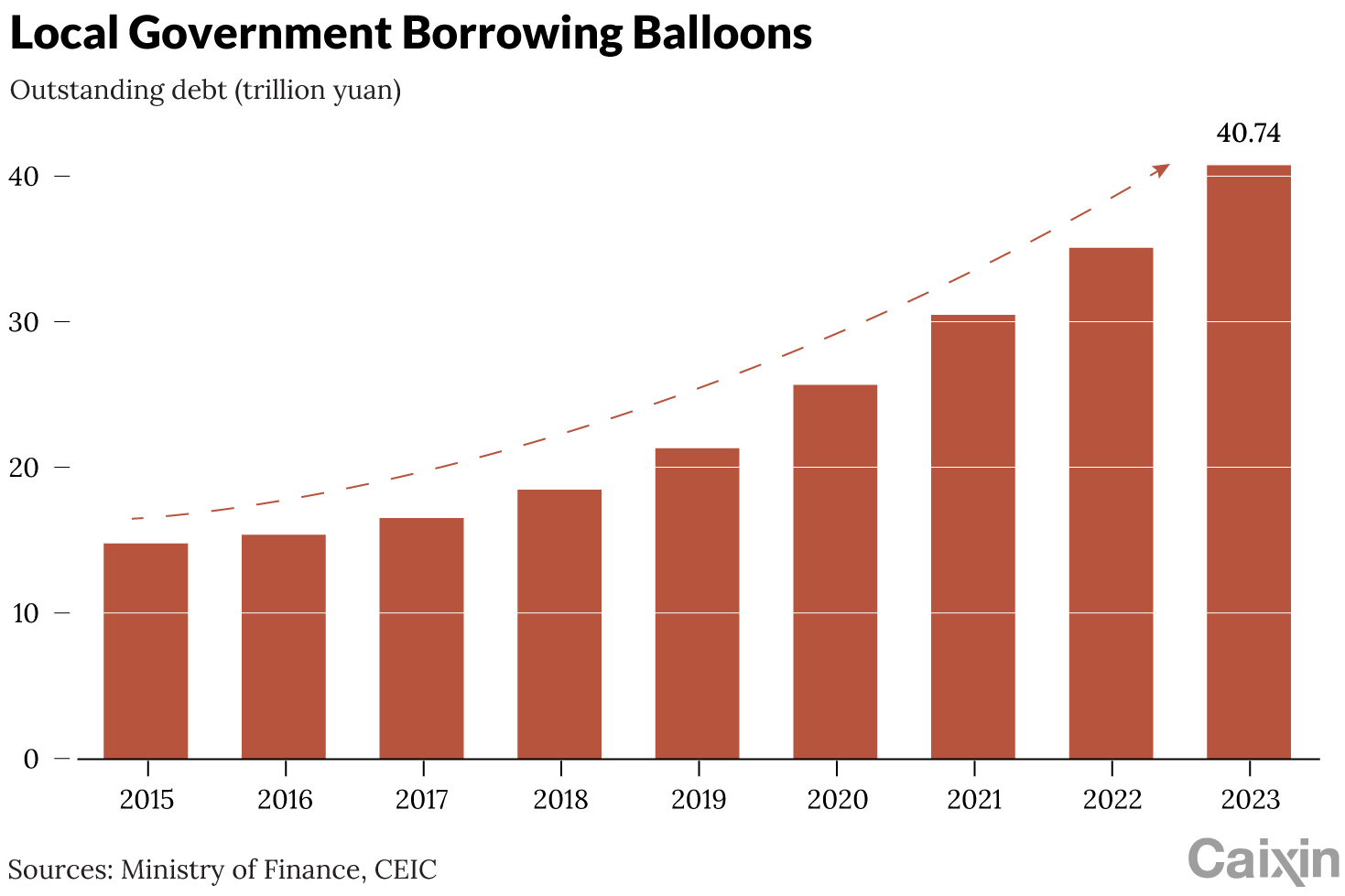

But the property crisis was just the visible tip of a much deeper structural problem. China's local governments have accumulated trillions in debt, much of it hidden through complex financial vehicles. With land sales typically accounting for over 40% of local government revenue, the property crash created a debt spiral that forced cities to slash basic services with some even suspending heating for residents in winter.

Banks, facing pressure from bad loans and regulatory uncertainty, began rationing credit away from private companies and toward state-owned enterprises (SOEs). By 2024, Chinese banks were allocating 80% of new loans to SOEs, despite these state-owned giants showing consistently higher levels of bad debt than private firms.

The numbers are staggering: SOEs received loans at annual rates as low as 1.5%, while private companies faced either rejection or punishing interest rates. Some SOEs literally borrowed cheap money and deposited it in other banks at higher rates, earning risk-free arbitrage while private entrepreneurs like Bi, Liu, Zeng, and Wang watched their credit lines disappear.

When Trust Becomes a Luxury You Can't Afford

Many successful Chinese companies operated on relationship-based business models: prepayments, chain financing, and personal guarantees that worked beautifully when everyone believed in tomorrow being better than today.

But trust, once broken, creates cascading failures. When customers stop prepaying, suppliers demand cash upfront. When banks freeze credit lines without warning, personal guarantees become death sentences. When regulatory audits can appear overnight and seize assets arbitrarily, long-term planning becomes impossible.

The entrepreneurs who died weren't just facing financial pressure, they were operating in an environment where success itself had become suspicious. China's anti-corruption watchdog can detain individuals without legal oversight, turning business disputes into political purges. Harsh environmental fines, frozen accounts, and arbitrary audits can destroy companies overnight, regardless of actual wrongdoing.

Unlike businesses in the United States or Europe, Chinese private companies lack meaningful bankruptcy protection. When Western entrepreneurs face insurmountable debt, they can restructure, reorganize, or liquidate through established legal frameworks. Chinese entrepreneurs face a binary choice: success or total destruction, with no middle ground and no legal safety net.

The Global Earthquake Waiting to Happen

Here's why the suicide of four Chinese business leaders should keep executives in boardrooms from Detroit to Stuttgart awake at night: China remains the world's manufacturing hub, accounting for 28% of global manufacturing output and controlling critical supply chains across industries.

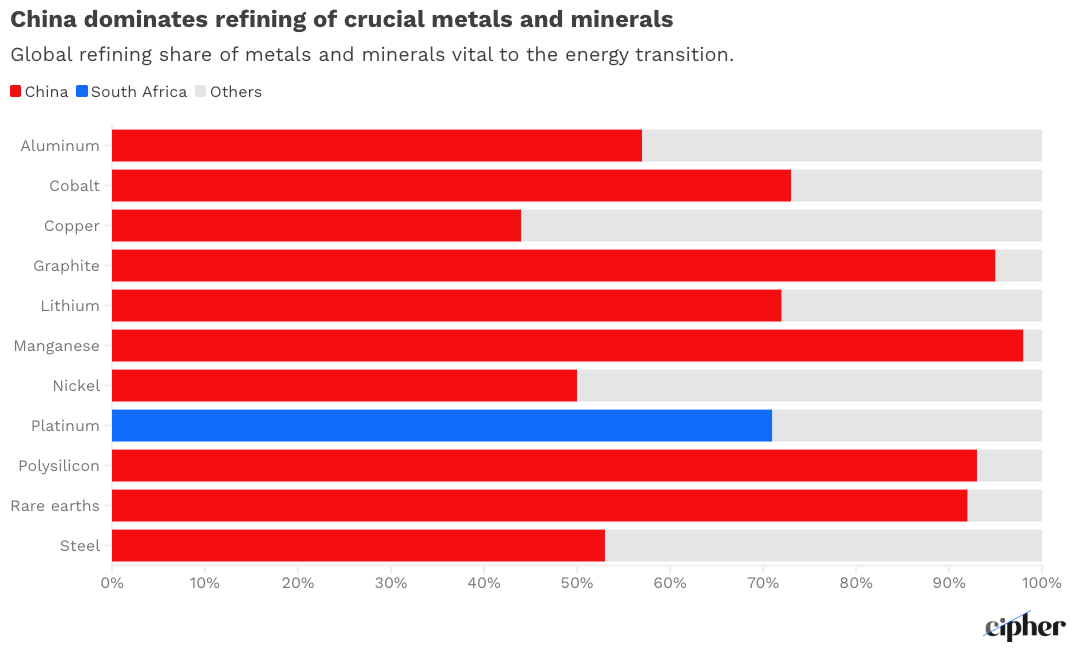

China has mastery over every step of critical mineral production, from mining and extraction to purification and finishing. In semiconductors, China accounts for 16% of worldwide production capacity, expected to hit 28% by 2030. China controls more than two-thirds of global polysilicon production compared to the U.S.'s 9%.

Alternative manufacturing hubs like Vietnam, India, and Mexico are becoming more competitive, but they lack China's integrated ecosystem of suppliers, logistics, and skilled labor. Companies implementing "China+N" strategies, where companies maintain Chinese operations while developing alternative sources, face the challenge of replicating decades of industrial development in countries with vastly different capabilities.

Meanwhile, the confidence crisis among Chinese entrepreneurs threatens the innovation and dynamism that made China's manufacturing sector so formidable. When the most capable business leaders are choosing death over continuing to operate, when trust has collapsed and credit has been weaponized, the entire system becomes fragile.

The Unspoken Truth

The deaths of Bi Guangjun, Liu Wenchao, Zeng Yuzhou, and Wang Linpeng weren't just personal tragedies, they were canaries in the coal mine of a system eating its own children. Each represented a different sector of China's economy, but they all faced the same impossible equation: a shrinking market, disappearing credit, regulatory uncertainty, and a political environment where private success had become a liability.

Their suicides were censored from trending topics on Chinese social media for at least 24 hours, a telling detail about a regime that understands the symbolic power of these deaths. When successful entrepreneurs choose death over another day in business, it sends a message that no amount of propaganda can suppress: something fundamental is broken in the Chinese dream.

The world spent decades building supply chains around Chinese manufacturing prowess and entrepreneurial energy. If that foundation is crumbling from within, the reverberations will be felt in every economy, every industry, and every supply chain on Earth.

The question we must all ask is how far the cracks will spread before the world finds a new equilibrium. And whether that new equilibrium will arrive through managed transition or catastrophic collapse.

The silence after Zeng Yuzhou's fall lasted just long enough for algorithms to scrub the story from trending topics. But silence, as these four deaths prove, can be the loudest scream of all.